With lingering overstock issues eating into the cash flow of corporations for two consecutive years, the bicycle industry is looking for a turn of the tide. While companies resort to various measures in order to reduce operational costs, some encouraging indicators are starting to emerge.

Back in 2022, business looked promising. Many companies reported new turnover and profit records that year and, as such, kept producing at maximum capacity, expecting the boom to continue. But the tide had already started to turn midway through 2022. Global unrest, like the war in Ukraine, was one major cause of concern, as were escalating trade conflicts between the United States and the European Union on one and China on the other side. The escalation of the Near East conflict in October 2023 was another worrying factor. Add in rising costs for raw materials, energy and transport and you end up with a toxic mix for the industry’s globally operating supply chain. At the same time, consumer sentiment plummeted to rock bottom due to inflation and the cost-of-living crisis. With a few notable exceptions, such as high-end road bike makers Pinarello and Colnago, most companies within the bike industry saw both their turnover and their profits decline year-on-year in 2023 and into the first half of 2024.

No lack of bad news

There has been no lack of bad news, either. Fitch repeatedly downgraded the credit rating of the Accell Group, one of the largest players within Europe’s bicycle industry, reaching a ‘substantial credit risk’ CCC- status this summer. To lower costs, the Accell Group shut down one of its factories in the Netherlands, cutting 150 jobs as a consequence. Pierer New Mobility, one of the fast-rising stars of the industry, also ran into serious issues first with its motorbike and then with its bicycle business. Specialized and Trek, among the most prestigious brands in the U.S., have been cutting their respective staff by up to 10 percent. Other companies reduced their staff to lower operating costs this year, including Hayes Performance, Rad Power Bikes, GoPro and Quality Bicycle Products.

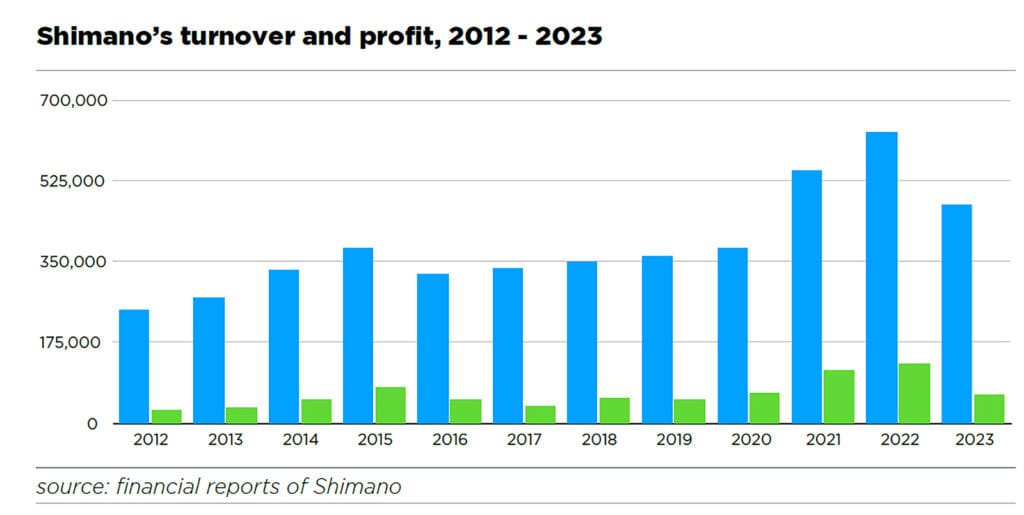

A useful indicator to rate the state of the bicycle industry are the quarter results of publicly traded companies with a strong dependance on OE sales, such as Shimano, Fox Factory and Schwalbe. As the leading supplier for quality brakes and drivetrain components, Shimano saw its turnover drop by 30 percent year-on-year in 2023. The good news is that the decline in turnover slowed to 22 percent in the first quarter of 2024 and 18.9 percent in the second quarter, although turnover still was down by 20.7 percent year-on-year for the first half of 2024. While the erosion in turnover is seemingly slowing down, this at least partly is due to a low base of comparison. Similarly, the turnover of Schwalbe as a key supplier of tires and inner tubes was down by 30 percent in 2023.

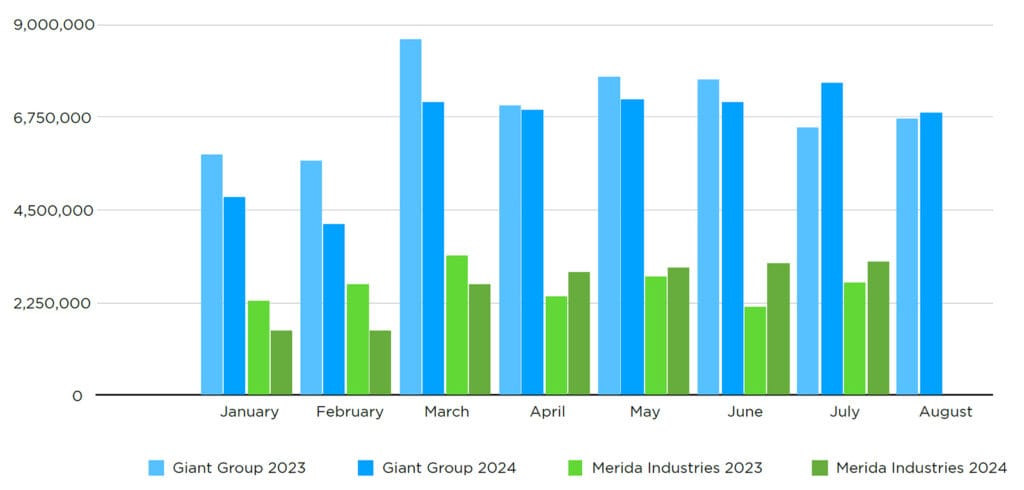

Promising numbers from Giant and Merida

This may be the time to invoke the words of a certain Richard Nixon. When campaigning as incumbent U.S. president in the early 1970s, he resorted to higher mathematics and to the third derivative to defend his administration’s track record in fighting inflation, arguing that “the rate of increase of inflation was decreasing.” On that basis, Shimano could now argue that the rate of decrease of their business has been decreasing as of late. Things look different with Fox Factory, which took an even harder hit. In 2023, the turnover of its bicycle-related Special Sports Group division dropped by 40 percent year-on-year. Halfway into 2024 the situation had not improved yet with the turnover still down by 39.3 percent year-on-year.

The numbers of Taiwan’s largest publicly traded bicycle manufacturers, Merida Industries and the Giant Group, look more promising. The Giant Group saw its turnover decline by 16.4 percent year-on-year in 2023 to NT$ 76.96 billion (US$ 2.44 billion). This negative trend grew even stronger in early 2024 when the turnover dropped by 20.25 percent year-on-year in the first quarter. From there, however, things seemed to have been improving, with the decline in turnover standing at 12.5 percent at the end of the second quarter, and the months of July and August posting better numbers than a year before. As a result, the Giant Group was only trailing last year’s numbers by 7.4 percent at the end of August, a sign that rock bottom may have been passed, even though higher operational costs and discounting did eat into profits.

The numbers of Merida Industries looked even more bleak at the end of 2023 as its turnover had declined by 26.4 percent to NT$ 27.17 billion (US$ 861 million). This negative trend continued into 2024, culminating in February when the monthly turnover was down by a staggering 41.3 percent year-on-year. But things started to look better in March, and since April, Merida Industries has seen a higher turnover than the year before. As a result, turnover was only trailing last year’s numbers by 0.81 percent at the end of July. Unfortunately, no official numbers were available for the month of August as of press time. But, if this positive trend continues to the end of the year, the turnover of Merida Industries may well be back to a moderate growth year-on-year. And that would be good news indeed.