Many market participants in the DACH (German-speaking) countries started the 2024 season with full inventories. The good news is that after a solid spring, the situation seems to be easing – at least a little. SHOW DAILY spoke with experts from the bicycle industry in Germany, Austria, and Switzerland.

The famous German Schlager song “Wann wird’s mal wieder richtig Sommer?” is a version of the American hit “City of New Orleans” rewritten as “When will we have a proper summer again?”. The sentiment matches the current industry mood in Germany, Austria, and Switzerland. Like most global markets, the bike business in these countries is dealing with the repercussions of the coronavirus pandemic — supply chain issues, the resulting bullwhip effect, and the demand fluctuations that have led to overstocked warehouses and declining sales over the past two years.

Germany: first revenue decline since 2006

Market data presents a mixed picture, yet the situation is not as gloomy as one might think. For example, in a recent market report, the research institutes IFH Köln and BBE Handelsberatung found that the German bicycle market recorded its first revenue decline since 2006. After peaking in 2022, when the German bicycle market achieved a total revenue of around 10.8 billion euros, analysts recorded a 5.2% decrease in 2023 compared to the previous year. “High inventory levels at bicycle dealers are leading to significant price reductions to sell the stock. This is currently being felt primarily by manufacturers, who are experiencing order declines,” comments Christoph Lamsfuß, Senior Consultant at IFH Köln. However, he also says: “In the coming years, the market will stabilize and show consistent growth” – a statement that suggests sentiment is becoming more positive in the German bicycle market.

The highly respected market data from Germany’s ZIV (Zweirad-Industrie-Verband) confirm these findings: after the all-time high in 2022, the total production volume of bicycles and e-bikes levelled off in 2023 by 11% – down to 2.3 million units. Despite this decline, there are optimistic signs on the horizon. Katharina Hinse, Head of Economic and Industrial Policy at ZIV, comments: “The 2024 season has started quite well in terms of end-customer demand. The weather in Europe is playing into our hands, making consumers eager to ride bicycles,” she said.

Regarding supply chain issues, overstock, inflation, and consumer sentiment, Hinse remains cautiously optimistic. “We expect the general situation in the industry to normalize by the end of this year. However, some companies may still struggle with high inventory levels and economic downturns into the following year. Conversely, some companies are already reporting a recovery and even significant revenue increases, indicating a heterogeneous situation.” Looking ahead, Hinse has positive expectations for the German bicycle market in 2025. “The bicycle industry is a future-oriented sector and will soon again generate profits for companies.”

A perspective on the German bicycle retailer landscape is provided by Uwe Wöll from the Verbund Service und Fahrrad (VSF): “The season so far in 2024 has been mixed,” he says. “Some retailers report a good first quarter, while others face significant and sometimes inexplicable sales declines. On average, however, we are slightly above last year’s level,” he continues.

Addressing the economic developments, Wöll notes the major challenge now is to effectively market and professionally sell products. “This was largely unnecessary in recent years and needs to be re-emphasized,” he states. Wöll also highlights the importance of liquidity planning and inventory management during this period. Despite these difficulties, the expert remains optimistic about the market’s recovery, expecting stabilization by this summer. “Inventory levels are decreasing, and cash flows are slowly improving. The consumer sentiment towards bicycles remains positive.”

Austria: encouraging news from retailers

In Austria, the story is much the same as its bigger neighbor. About 421,000 bicycles were sold to the Austrian sports and bicycle retail trade in 2023, according to the annual market analysis by the Verband der Sportartikelerzeuger und Sportfachhändler Österreichs (VSSÖ). In 2022, it was 506,000 vehicles – a decline of 16.8%, bringing the market back to the level of 2019. “In 2020, 2021, and 2022, the sales volume was at an exceptionally high level,” says Hans-Jürgen Schoder, spokesman for the industry organization ARGE Fahrrad. “This disproportionate growth was mainly due to pandemic-related catch-up effects, leading to high inventory levels in 2022 and 2023,” he explains.

Meanwhile, the sports and bicycle retail trade reports satisfactory sales and revenue figures with some exceptions, according to Schoder. “So far, retail sales in 2024 have been satisfactory. Even at the start of the season before Easter, speciality retailers were able to sell well,” says Schoder, who also provides details: “racing bikes, gravel bikes, folding bikes, and cargo bikes are selling very well. There are already models that are sold out and have delivery problems, while others still have overstock. It also depends on the brands. A-brands are in high demand, while B or C brands are struggling with sell-through,” he observes.

Inflation easing this year is likely to have a positive effect: “The consumer climate in the bike sector is quite positive: our retailers report positive sales figures in the first three months of this year, especially over the Easter sales. By 2025 at the latest, we expect the bicycle market to stabilize for the industry as well.”

Switzerland: early signs of recovery

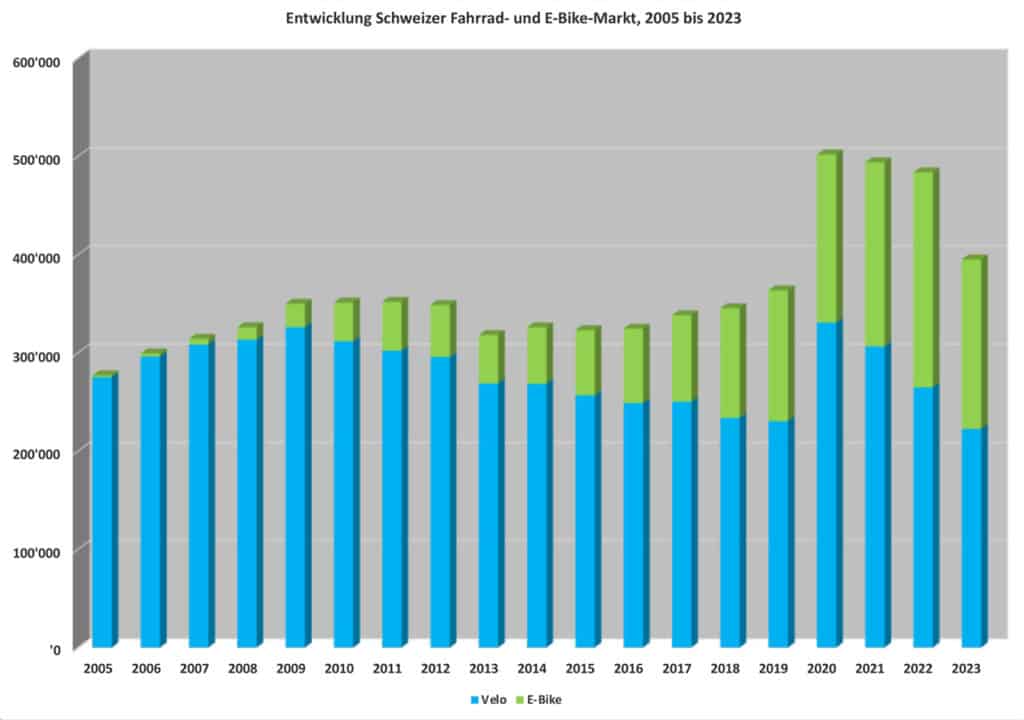

In Switzerland, the season also started with still-full warehouses. According to the annual survey by the Swiss bicycle suppliers’ association Velosuisse, in total 395,036 bicycles and e-bikes were delivered to the local bicycle trade in 2023. This is around 100,000 vehicles fewer than in the pandemic years 2020 to 2022.

However, industry and economic experts were not surprised by this. In 2022, consumer sentiment had already cooled significantly due to war, interest rate hikes and inflation, as the record quantity of 218,730 e-bikes was delivered to the market far too late. “A nice spring in 2023, which could have eased the situation, did not materialize. When summer came, it was so hot that the desire to ride bicycles evaporated. So, it is only logical that fewer bicycles and e-bikes could be sold last year,” summarizes Martin Platter from the Swiss Office for Bicycles & E-Bikes.

As a result of the overflowing stocks at the beginning of 2024, Platter describes a shift from a trade-oriented to a customer-oriented system, where customers benefit from discount battles. “When discounts of 20 to 30% are already being advertised at the start of the season, it says a lot about the inventory levels in the bicycle shops. For end customers, it’s a paradise. For retailers, less so,” explains the expert. Platter adds: “Margins are under pressure at all levels. The trade relationships between suppliers or manufacturers and retailers are also affected. For example, when major brands lower their prices in their end-customer webshops so much that they are below the purchase price for the retailer and the retailer still has a full inventory, then this leads to friction.”

However, there are signs of relief in Switzerland. “For high-demand products such as lightweight gravel bikes and lightweight e-bikes at reasonable prices, there are already supply shortages again. This is due to the restraint in the last pre-order, despite a rather poor spring in terms of weather,” says Platter. “The standout last year were the S-Pedelecs, which were the only category to increase in a market that was significantly declining overall,” he reports. Therefore, his general outlook for the Swiss bicycle market is positive: “Cautious, but not overly pessimistic. The bicycle has potential. This allows us to look confidently into the future. Especially since the product pipeline in the bicycle industry is well-stocked and the new lightweight drives have given fresh momentum to the e-bike movement.”

Experts expect normalization in 2025

The takeaway from this survey is that markets in the DACH region are beginning to show signs of recovery. All the experts surveyed agree that the situation should return to normal by 2025 at the latest – in Germany, Austria, and Switzerland. At least when it comes to the economic situation in the bicycle industry, this also provides a preliminary answer to the question posed by the German Schlager song “Wann wird’s mal wieder richtig Sommer?” – “When will we have a proper summer again?”.