Two years ago the market for quality bicycles tanked, provoking a lot of order cancellations. The global industry is still struggling with a toxic combination of high inventory levels and rising costs that eat into margins. Is there some light at the end of the tunnel?

With the pandemic-induced boom and the collapse of consumer sentiment due to wars in Ukraine and the Middle East, the bicycle industry was hit by two black swan events in rapid succession. This has thrown supply and demand badly off balance, filling up warehouses around the globe. One question has been keeping decision makers throughout the industry on their toes ever since: how long will they have to struggle with crushingly high inventory levels that create additional costs for storage, provoke wide-spread discounting, cut into the revenue and erode margins along the entire supply chain? And how can companies deal with low liquidity levels caused by reduced turnover at lower margins against the backdrop of rising costs for rents, salaries, power and the payment of interest rates?

Taiwan’s exports take a blow

Scaling back production planning was the first measure taken by many bicycle brands. And a natural reaction, given the overstock issues that are still evident in the export statistics of Taiwan, a key supplier to the industry. Exports of e-bikes dropped by 33 percent in unit terms last year following a record-breaking year in 2022. But since the average unit price went up by 17.8 percent, the loss in value only stood at 21.9 percent. Taiwan’s exports of conventional bicycles took a harder hit, seeing a decline of 32.2 percent in units and of 26 percent in value. Worst-off were parts and components however. In this segment Taiwan’s exports dropped by 51.6 percent in weight and by 41.4 percent in value. The import of parts and components saw an even stronger decline at 54.4 percent in weight and 32.3 percent in value.

The export data for the first quarter of 2024 show that the trend is turning somewhat. The same pattern of a dismal year 2023 followed by a slighly better first quarter of 2024 can be seen when looking at last year’s numbers of Giant Group and Merida Industries, some of the biggest bicycle and e-bike manufacturers. The tide seems to be turning, as shipments are at a lower level than the boom years but still at a higher level than before the pandemic. Unsurprisingly some key suppliers to the bicycle industry have been facing similar issues. Shimano saw its revenue drop by 29.5 percent year-on-year, while the turnover of the Special Sporting Goods division of Fox Factory was a massive 43.5 percent below 2022’s numbers. Schwalbe also saw its turnover reduced by 30.5 percent in 2023.

Factories running at a fraction of their capacity

These numbers show the extent of the down-scaling of the production as the losses in turnover of these key suppliers translate to roughly one third less bicycles being produced. One obvious consequence of this reduction is factories running at a fraction of their maximum capacity along the entire supply chain. In this regard, little had changed from November 2022 to September 2023 in large factories in Taiwan that were running at 30 to 40 percent of their capacity while having to resort to makeshift warehouses to store all the paletted finished goods. One serious challenge in this situation is to keep employees on board despite reduced working hours and lower incomes. In Taiwan, some companies finished their contracts with migrant workers first to cut costs, using this part of their staff as a buffer.

The situation was similar when visiting various factories in Southern Vietnam right after the Taipei Cycle Show in March 2024 – some of them still under construction. As a frame maker Astro Tech has invested in a new factory in Vietnam that is replacing its original factory built in 2000. Astro Tech’s General Manager Samuel Hu explained: “From 2020 to 2022 our factories in Vietnam were running at two shifts to cover the demand. Now we are back to one shift, and the factory is currently running at 30 percent of its capacity.” Manufacturers in Far East are not the only ones to feel the pinch as the production of bicycles and e-bikes in the EU was also down year-on-year in 2023.

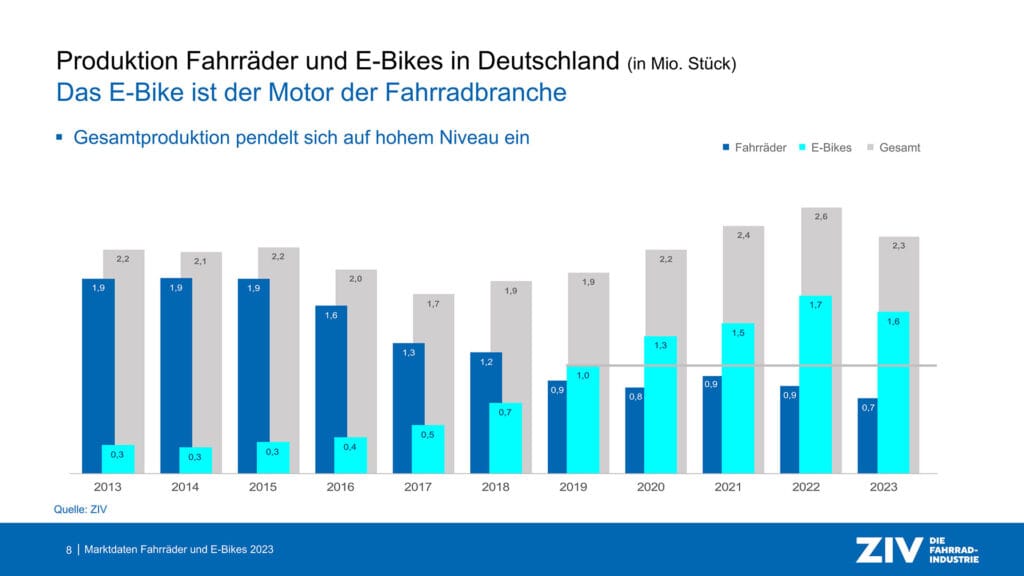

Production down in Europe as well

The numbers presented by the Zweirad Industrie Vereinigung (ZIV) as Germany’s bicycle industry association show that the production of e-bike and conventional bicycles by its members was down by 11 percent to 2.3 million units year-on-year. The production of e-bikes only dropped by 6 percent to 1.6 million units, but production of conventional bicycles was down by 22.2 percent. The official export and import statistics provided by Eurostat also show that the exports of e-bikes and conventional bikes from the EU trade block dropped by 10 percent in value with the imports declining by 21 percent. In unit terms e-bike exports dropped by 21 percent and imports by 27 percent while conventional bicycles saw a drop of 17 percent in exports and 34 percent in imports.

These numbers show the effect of high inventory levels, but they also show that e-bikes are less affected than conventional bicycles. One general pattern is that manufacturers that heavily rely on model years and the volume market were hit by the downturn in demand much harder than brands that focus on the upper segments of the market and offer platforms that only see slight changes from one year to the other. Italian premium road bike brands Pinarello and Colnago both bucked the trend in 2023 and reported robust growth rather than a downturn. Meanwhile mountain bikes without electric assistance were a hard sell and were discounted most aggressively. While Kona Bikes made headlines with their “buy one get one for free” offer, Specialized essentially went the same way when offering discounts of up to 60 percent on select models for a limited time.

A recovery in the making?

At these discount levels, nobody is making money but since the existing overstock is losing value by the day while causing additional costs, companies are taking drastic measures to turn some inventory into cash. Trek made headlines when it announced to cut operational costs by 10 percent during the Taipei Cycle Show, and Scott Sports got a massive US$ 150 million loan from its majority owner Youngone Corporation to avoid cashflow issues. Meanwhile the rating agency Fitch downgraded the Accell Group to a CCC rating, adding to the woes of this large corporation that has been plagued by high inventory levels and low liquidity and has been cutting costs and staff for quite a while now. Swiss E-bike pioneer Flyer had to cut its staff from 200 to 120 persons in late September 2023, essentially getting its staff size back to where it had been in the Spring of 2021.

Is there anything positive amid all of this bad news? Looking forward, the tide seems to be turning on various fronts: according to b2b portal nieuwsfiets the turnover of the Dutch bicycle trade was up by 5 percent year-on-year in Q1 2024, and the drops in Taiwan’s e-bike exports and the EU’s e-bike imports seem to have stabilised. French sporting goods giant Decathlon expects the situation to improve by Q4 of this year, and Young Liu, co-CEO of the Giant Group, hinted at a change of the trend in Q3 of this year at a press conference for domestic media held at the Taipei Cycle Show. According to the news portal Focus Taiwan, one large player from the bicycle industry saw orders stabilize and reinstated full-time hours for about 200 workers in mid-May as well. With the wars in Ukraine and the Middle East and trade conflict between China, the US and the EU, there are still factors beyond the control of the bicycle industry that complicate the road to recovery.